Personal Lines of Credit vs. Personal Loans: How to Differ

Many consumers experience temporary financial issues and search for an appropriate lending solution to help them fund their urgent money needs. Getting a personal loan or a personal line of credit are two widespread options to choose from. They both may be unsecured so the borrower won’t need to pledge collateral.

On the other hand, these borrowing solutions are functionally different. How do these options differ? What is the best solution in your case? In this article, we are going to discuss how to select the most suitable option and solve your financial problems.

What Is a Personal Loan?

In general, many lending solutions are similar as they serve the same purpose to provide you with additional cash to cover immediate costs and unforeseen expenses.

A personal loan means a type of lending solution issued to the borrower with a fixed amount of cash given in the lump sum. The payments are done according to the repayment schedule and they may be done weekly, bi-weekly, semi-monthly, or monthly.

Borrowers may obtain this fast money borrowing at a variety of crediting institutions including local banks, credit unions, or alternative online creditors.

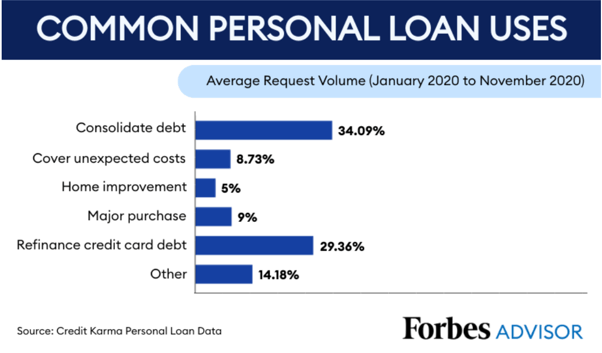

You may utilize a personal loan to:

- Fund your wedding

- Finance a funeral

- Make a big-picture purchase

- Pay down credit card debt

- Cover student loan debt

- Debt consolidation

What Is a Personal Line of Credit?

This lending solution differs from a personal loan as it works more like a credit card. A personal line of credit may also be secured or unsecured. This is a revolving credit line that has a variable interest rate and a credit limit.

If you have a sudden auto repair and you don’t know the total cost of it, this lending solution may be a great choice. The borrower has to pay interest only on the sum of the credit line they take out. The payments will change due to variable interest rates. You may obtain a personal line of credit at a variety of crediting institutions including local banks or alternative lenders.

You may utilize a personal line of credit to:

- Fund emergency situations

- Cover home improvement project

- Finance an auto repair

- Support your monthly needs in case of irregular income

How Do They Differ?

Though there are some similarities between these two lending options, they have different applications. They differ in the way funds are issued to the borrower, interest rates, as well as the repayment process.

Typically, personal loans are given at a lower interest rate. It may be as low as 10% if the client has an excellent credit history. Credit cards or personal lines of credit may come at 16% and higher.

According to the FRED economic research, the average APR for a two-year personal loan issued by the local bank is 9.58% but conventional banks have strict eligibility criteria and require excellent credit.

| Personal Loan | Personal Line of Credit | |

| Type of disbursement | Lump-sum | Reusable credit (you get a portion of cash at a time) |

| Type of credit | Installment | Revolving |

| Interest rate | Fixed | Variable |

| Secured or Unsecured | Can be both | Can be both |

| Loan amount | $1,000 – $100,000 | $5,000 – $100,000 |

| Extra fees | May come with application fees, origination fees, prepayment/late charges | May come with late fees, overdraft charges, annual fees |

| Minimum credit score | 580 | 670 |

| Repayment Options | Weekly/bi-weekly, semi-monthly, monthly. Two to seven years | Varies and is ongoing. You pay interest at the end of each term |

Your credit rating plays an important role in choosing the desired lending solution. Many service providers perform a hard credit inquiry to verify clients’ banking and private information. A hard credit check may harm your rating and credit history.

So, if your rating is less-than-perfect you may need some time to search for a suitable lender first and ask if they conduct a soft credit pull.

There is also a difference in money disbursement. If you obtain a personal loan you will get a lump sum of cash straight away with a certain repayment schedule. If you lack cash in the nearest future you will have to request another loan.

On the other hand, a personal line of credit allows the borrower to withdraw money on a continuous basis until they reach a predefined credit limit. It may be more suitable when you aren’t sure about the total costs.

Which Option Is Better?

Depending on your current financial situation, you may need a certain lending solution. It’s great that there is an option to request an unsecured personal loan or line of credit. It means you won’t need to secure the debt with your valuable assets such as an auto or a house. This way, the borrower faces fewer risks in the future.

- Choose personal loans: when you need a particular sum as a one-time expense for covering urgent costs, debt consolidation, or an expensive purchase. The money is returned to the lender in regular fixed payments.

- Choose lines of credit: when you don’t know the exact amount of cash you will need to cover ongoing expenses. Personal lines of credit give more flexibility to the borrower with a chance to obtain as much as they currently need and pay the monthly balance with a variable interest rate.

Bottom Line

In conclusion, it pays to be careful with the lending solution you select. Don’t rush with your decisions and take some time to do some research. Compare lending offers and quotes of several lenders until you find the most affordable contract to sign. Review the rates and lending conditions of the offer and decide which option suits your current financial needs.

There is no one-size-fits-all lending solution so you should take into account your present situation, urgent money needs, as well as your credit history. Define which offer you are eligible for and choose the best deal.

839GYLCCC1992

Leave a Reply